The peptide market has exploded from bodybuilding forums to GLP-1 weight-loss clinics to research-chemical suppliers but almost every operator in this space runs into the same wall early on: getting approved for a merchant account. Mainstream processors like Stripe, PayPal, and Square routinely decline peptide sellers, and even when an account slips through initial underwriting, it’s often frozen or terminated once a manual review flags the product category.

This guide breaks down why peptide businesses are treated as high-risk, what card networks and banks actually expect in 2026, and the concrete steps that improve your odds of getting and keeping a stable merchant account.

Why Peptide Websites Are Classified as High-Risk

Payment processors don’t single out peptides arbitrarily. Underwriters weigh a handful of specific risk factors before deciding whether to approve an account.

Chargebacks. Peptide merchants tend to see dispute rates well above normal e-commerce benchmarks, largely because customers misunderstand how a product is meant to be used, question its efficacy, or simply don’t recognize the charge on their statement.

Regulatory ambiguity. Peptides increasingly fall under expanded FDA scrutiny as compounded substances, and several have been flagged as carrying significant safety considerations when sold outside a clinical framework. That ambiguity makes banks nervous about long-term liability.

Card network monitoring. Mastercard’s risk-assessment programs specifically flag unapproved pharmaceuticals, research peptides, and nutraceuticals as elevated-risk categories, and enforcement has tightened further in 2026 to apply stricter controls over research peptide accounts specifically.

Put together, these factors mean a peptide site isn’t judged only on its own transaction history it inherits the risk profile of the entire category.

Why Stripe, PayPal, and Square Keep Shutting Peptide Merchants Down

A common and costly pattern in this industry: a merchant signs up with a mainstream processor, gets approved automatically because the underwriting bot doesn’t catch the edge case, and starts processing normally. Weeks or months later, a manual review flags the product category, the account is terminated, and any available balance is frozen often for 90 to 180 days while the processor assesses its liability exposure.

Platform terms of service add a second layer of difficulty. Many major e-commerce platforms prohibit selling substances that require a prescription for human use, which limits which payment gateways will even integrate with a storefront in the first place.

If a termination happens and the processor reports it to Mastercard’s MATCH file (Member Alert to Control High-Risk Merchants), the consequences extend well beyond that one account. Merchants on the MATCH list typically struggle to get approved by any processor for years afterward.

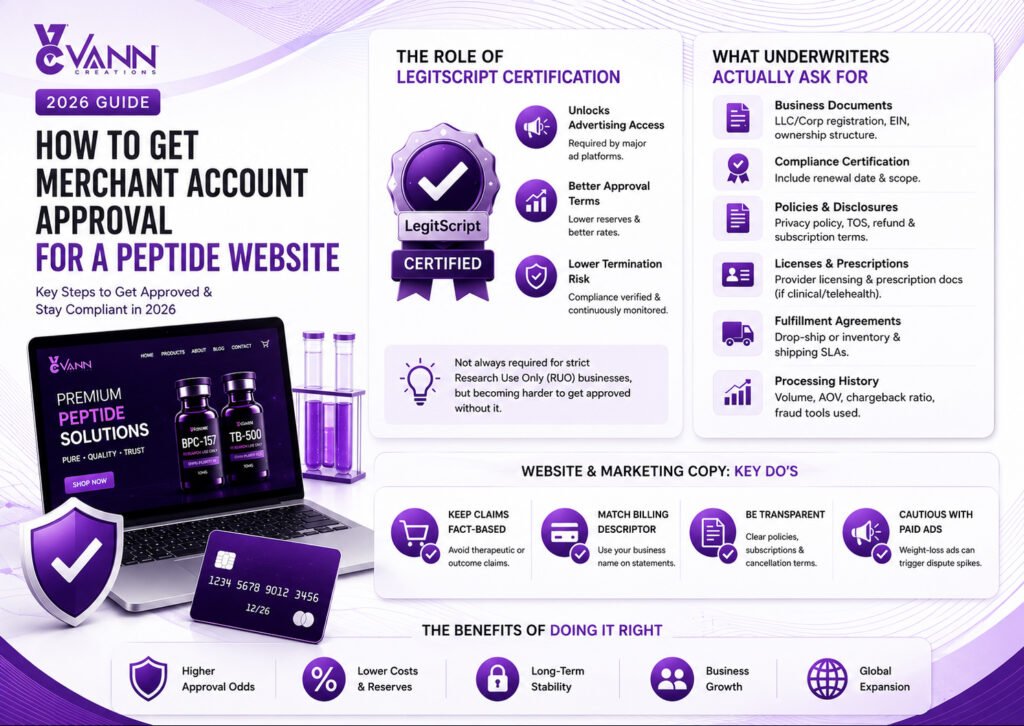

The Role of LegitScript Certification

For an increasing share of peptide and GLP-1 businesses, LegitScript certification has moved from “helpful” to effectively mandatory. LegitScript is a third-party compliance verification company; major ad platforms and card networks reference its database to decide which healthcare-adjacent merchants are allowed to advertise or process payments.

What certification actually gets you:

- Advertising access. Major ad platforms reject healthcare-adjacent advertisers outright without it, with no manual-review workaround.

- Better underwriting terms. Certified merchants tend to see improved approval odds, lower reserve requirements, and more competitive processing rates.

- Lower termination risk. Because compliance is independently verified and continuously monitored, banks have less reason to shut an account down mid-stream.

Certification reviewers specifically look for red flags such as missing prescription requirements, broad catalogs built around performance or weight-loss claims, and no safeguards confirming professional or clinical use patterns associated with unapproved human consumption.

That said, certification isn’t universally required. Businesses operating strictly under a research-use-only (RUO) model, coded correctly under the appropriate merchant category code, can sometimes secure domestic processing without it though banks that accept RUO framing without prescription or clinical oversight are becoming harder to find as 2026 underwriting standards tighten.

What Underwriters Actually Ask For

Before you apply anywhere, assemble the documentation a high-risk underwriter will want to see:

- Business formation documents LLC/Corp registration, EIN, and ownership structure.

- Compliance certification (where applicable), including the renewal date and the exact scope it covers.

- Complete policy pages privacy policy, terms of service, refund policy, and subscription cancellation terms, all clearly linked from checkout.

- Provider licensing and prescription documentation, if you operate a clinical or telehealth model.

- Fulfillment agreements drop-ship or inventory arrangements and shipping SLAs.

- Processing history, if you have any — average ticket size, monthly volume, card-not-present percentage, chargeback ratio, and the fraud tools you already use.

Before you submit anything, walk through your own checkout as a customer would. Underwriters do the same thing, and inconsistencies between your marketing copy and your actual product descriptions are one of the fastest ways to get declined.

Website and Marketing Copy: The Details That Sink Applications

Even subtle wording can trigger a compliance flag. Phrases like “supports recovery” or “promotes growth” read as therapeutic claims to a reviewer, even if you consider them casual marketing language. Underwriters and card-network monitoring tools generally want product descriptions to stay technical and research-oriented rather than outcome-oriented.

A few practical rules that consistently come up across high-risk underwriting checklists:

- Match your billing descriptor to your business name. Customer confusion about a charge is one of the biggest drivers of “friendly fraud” disputes in this category, and a mismatched descriptor makes it worse.

- Don’t pair “not for human consumption” disclaimers with consumer-facing checkout flows. Underwriters treat that combination as a classic red flag for undisclosed human use.

- Disclose subscriptions and cancellation terms transparently. Recurring billing without clear cancellation instructions is a well-documented dispute generator in this vertical.

- Be cautious with paid social campaigns, particularly for weight-loss peptides. Viral ad spikes without a strong post-purchase communication plan tend to produce dispute spikes that underwriters specifically watch for.

Choosing a High-Risk Processor

Once your documentation and website are in order, the processor you choose matters almost as much as the application itself. A few things worth evaluating:

- Explicit category acceptance vs. generic high-risk brokers. A processor that explicitly underwrites peptide and research-chemical merchants is a different proposition from a generic high-risk broker who might drop you after a later portfolio audit.

- Single-bank vs. multi-bank routing. A processor that routes transactions through only one acquiring bank creates a single point of failure; multi-bank arrangements offer more redundancy if one banking relationship sours.

- Reserve structures. Expect rolling reserves in the 5–10% range held for a set period (commonly around six months) as standard practice for this category.

- ACH/eCheck as a backup rail. Because ACH processing runs outside the Visa/Mastercard network entirely, it isn’t subject to the same card-network category restrictions which is why many peptide operators keep an ACH processor as a secondary channel.

- Redundancy from day one. Given how often accounts in this category get re-underwritten or terminated without warning, maintaining two active processing relationships rather than relying on a single provider is a widely recommended practice, not a contingency plan.

Quick Reference: Approval Checklist

- [ ] Business entity documents, EIN, and ownership structure ready

- [ ] LegitScript certification obtained or application in progress (if your model requires it)

- [ ] Privacy policy, TOS, refund, and cancellation pages published and linked at checkout

- [ ] Product descriptions reviewed for therapeutic or outcome-based claims

- [ ] Billing descriptor matches your legal/DBA business name

- [ ] Chargeback prevention tools in place (dispute alerts, fraud filters, velocity limits)

- [ ] Backup ACH/eCheck processing relationship established

- [ ] Two independent processing relationships live, not just one

The Bottom Line

Merchant account approval for a peptide website isn’t about finding a loophole it’s about building a documentation trail and a website that make an underwriter’s job easy. Card networks have made their monitoring stricter in 2026, not looser, so the businesses that treat compliance (certification where relevant, clean product copy, transparent policies, and dual processing relationships) as core infrastructure rather than an afterthought are the ones that stay approved long enough to actually grow.

This article is for general informational purposes and isn’t legal, financial, or compliance advice. Payment processing requirements change frequently and vary by processor, acquiring bank, and jurisdiction confirm current requirements directly with LegitScript, your card networks, and any processor before appying.